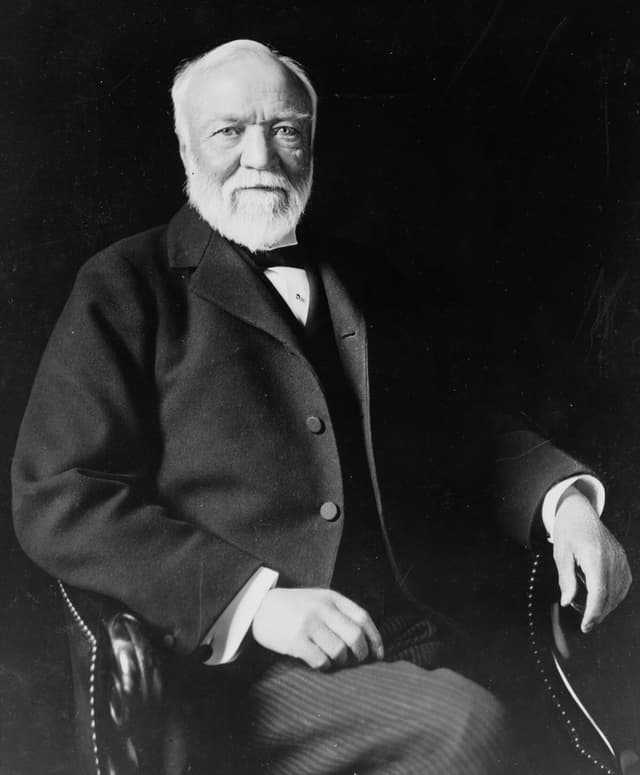

Andrew Carnegie

Carnegie Steel Company

A pioneering industrialist, Andrew Carnegie transformed the steel industry through his establishment of Carnegie Steel Company, which became the largest of its kind in the world by the late 19th century. Rising from humble beginnings as a bobbin boy earning just $1.20 per week, he leveraged technological advancements and strategic partnerships to amass a fortune, ultimately selling his steel company for $480 million in 1901. Carnegie's principles emphasized the importance of adapting to industry dynamics and recognizing the necessity of innovation, famously stating, "Cut the prices scoop the market the costs, and the profits will take care of themselves." His journey illustrates the critical balance between emotional attachment and rational decision-making in business, offering valuable lessons for entrepreneurs today.

Core Principles

competitive advantage

Identify where competitors are making mistakes and turn that into competitive advantage. Mediocrity in competitors creates opportunities for those willing to do things differently.

Carnegie was astonished to discover that manufacturers didn't know their costs. This ignorance meant waste was endemic. By introducing cost accounting, he gained a permanent advantage. What seemed like extravagant expenditure on systems actually revealed where competitors were hemorrhaging money.

“What fools we had been. But then there was this consolation. We were not as great as fools as our competitors.”

Use price reductions as a lever to increase market share and scale, knowing that lower costs create a virtuous cycle of volume growth.

Carnegie charged $65 per ton of rails while competitors charged $70, driving market share gains because he could produce at under $50. This allowed him to scale faster and further reduce costs through volume, creating a self-reinforcing competitive advantage.

“Cut the prices, scoop the market, watch the costs, and the profits will take care of themselves.”

culture

Involve younger team members or family in financial understanding. Transparency about income, expenses, and goals creates shared responsibility and teaches financial discipline early.

Carnegie's parents involved him in family finances from childhood. He knew what each family member earned and all expenditures down to the penny. This financial literacy informed how he later ran his business with strict cost accounting.

“My parents were wise and nothing was withheld from me. I knew every week the receipts of each of the three who were working. I also knew all the expenditures.”

Higher wages for respected, happy employees are an investment yielding big dividends, not merely a cost. Employee retention creates continuity and operational efficiencies that compound over time.

Carnegie believed that paying higher wages to workers who respect their employers and are content generates returns greater than the wage cost through reduced turnover, continuity, and efficiency. This contradicts the view that all labor costs are equivalent commodities.

“I believe that higher wages to men who respect their employers and are happy and contented are a good investment, yielding indeed big dividends.”

Transparency about your family's financial goal creates shared ownership. When everyone knows the target and their contribution to reaching it, motivation aligns across the household.

Carnegie's family set the specific goal of earning $300 per year to avoid dependence. By making this goal explicit and involving young Andrew in tracking progress, the family created unified purpose. Everyone understood what they were working toward.

“My thoughts at this period centered in the determination that we should make and save enough money to produce $300 a year, $25 monthly.”

Maintain a sense of gratitude and reciprocity toward those who helped you. Return their favor by helping others at the right moments in their careers.

Carnegie was deeply grateful to Colonel James Anderson for providing free library access. Decades later, when wealthy, he erected a statue to Anderson and built libraries in his name. He also repeatedly emphasized the importance of helping young people who showed promise, echoing the help he received.

“To Colonel James Anderson, founder of Free Libraries in Western Pennsylvania, he opened his library to working boys and upon Saturday afternoons acted as a librarian.”

finance

Focus obsessively on controlling costs, not revenue or profit. Profits and prices are cyclical, but cost savings are permanent.

Carnegie built his steel empire by tracking costs down to the penny, reinvesting savings into new technology, and constantly grinding expenses lower. Unlike competitors focused on revenue, he understood that cost control provided sustainable competitive advantage.

“Cut the prices scoop the market the costs, and the profits will take care of themselves.”

Implement detailed cost accounting systems to understand the true cost of each process and each person. This transparency enables management and continuous improvement that competitors cannot match.

Carnegie was shocked to discover that manufacturers did not know their costs until year-end accounting. He insisted on weighing and accounting systems that tracked cost by process and person. Managers resisted initially, but this system eventually gave him a massive competitive advantage.

“I felt as if we were moles burrowing in the dark. I insisted upon such a system of weighing and accounting being introduced throughout our works as would enable us to know what our cost was for each process.”

Apply the same oversight and accountability to large material costs as to small cash expenses. It is illogical to control small disbursements while allowing massive waste in materials and labor.

Carnegie observed that office managers would not trust a clerk with five dollars without oversight, yet they supplied tons of materials daily to mill workers without any accounting of what was returned or wasted. This inconsistency represented massive hidden costs.

“Owners who in the office would not trust a clerk with $5 without having a check upon him were supplying tons of material daily to men in the mills without exacting an account of their stewardship.”

Know your costs down to the penny. This knowledge provides a firm foundation for all business decisions and reveals where profits actually come from.

At age 13, Carnegie tracked his family's income and expenses. Later, when manufacturing iron, he was shocked to discover that manufacturers didn't know their production costs. He introduced cost accounting and discovered that almost half the waste in heating could be eliminated with new furnaces. Competitors didn't know this because they didn't track costs.

“If you knew your cost down to the penny, you were always on firm ground.”

Invest in your own business before external investments. The greatest returns come from improving your core operation, not from bank shares or distant enterprises.

Carnegie reinvested all profits into Carnegie Steel, improving furnaces, hiring chemists, implementing cost accounting, and acquiring complementary businesses. These investments created compounding returns that far exceeded external stock investments made by competitors.

“The true gold mine lies right in their own factories. My advice to young men would be not only to concentrate their whole time and attention on the one business and life in which they engage, but to put every dollar of their capital into it.”

focus

Focus your greatest talents on one dominant industry rather than scattering attention across multiple ventures. Put all eggs in one basket and watch that basket carefully.

Carnegie abandoned his diversified telegraph and oil investments to concentrate entirely on steel once he recognized it as the highest-leverage business. Frick similarly abandoned his coke-only strategy to eventually focus on steel operations.

“put all good eggs in one basket and then watch that basket”

Guard your attention as your most valuable asset. Do not own investments that require daily monitoring or distract from your core business, as attention fragmentation degrades decision-making.

Carnegie realized he compulsively checked stock prices every morning, splitting his attention from manufacturing. He resolved to sell all external investments and own no publicly-traded stocks. He believed a mind distracted by stock market fluctuations cannot judge wisely on manufacturing decisions.

“His mind must be kept calm and free if he is to decide wisely the problems which are continually coming before him. Nothing tells in the long run like good judgment and no sound judgment can remain with the man whose mind is disturbed by the mercurial changes of the stock exchange.”

Concentrate all resources on one business you can master completely rather than diversifying across many enterprises. The road to preeminent success requires putting all good eggs in one basket and watching that basket closely.

Carnegie withdrew from railway investments and concentrated entirely on manufacturing iron and steel. He believed most businessmen spread themselves too thin on bank shares and distant enterprises while missing the gold in their own factories. He made this a cardinal doctrine.

“I determined that the proper policy was actually to put all good eggs in one basket and then watch that basket. I believe the true road to preeminent success in any line is to make yourself master in that line.”

Keep your mind free from distraction so you can exercise sound judgment on the problems that matter. Divided attention prevents clear thinking on business essentials.

Carnegie realized that checking stock prices in the morning distracted him from his core business. He decided to sell all outside stocks and investments and focus entirely on steel manufacturing. He argued that sound judgment requires a calm mind, and the stock market creates mercurial thinking that undermines business decisions.

“Nothing tells in the long run like good judgment and no sound judgment can remain with the man whose mind is disturbed by the mercurial changes of the stock market.”

Focus on a single opportunity with complete commitment rather than pursuing multiple ventures simultaneously once you identify the right market.

After making investments in oil, iron, and bridges, Carnegie realized the greatest wealth opportunity lay in steel. He consolidated his focus entirely on steel production, abandoning his scattered approach to accumulate wealth in one dominant basket.

hiring

Employ experts and specialists, not just operators. Hiring chemists, engineers, and other trained professionals reveals hidden inefficiencies that operators alone cannot detect.

Carnegie hired chemists at blast furnaces while competitors thought this was extravagant waste. The chemists identified sources of waste in the process that operators missed. This single decision created a temporary monopoly on efficiency that lasted until competitors copied the practice years later.

“Had they known the truth, they would have known that they could not afford to be without one.”

Pay top dollar for exceptional talent in critical operational positions because the best people pay for themselves through efficiency gains.

Carnegie identified Henry Clay Frick as an exceptional operator and valued him highly enough to eventually make him chairman. He believed superior talent in manufacturing and operations justified premium compensation because their innovations and efficiency reduced overall costs.

“There is no labor so cheap as the dearest in the mechanical field.”

innovation

Technology adoption is not optional: it is survival. Firms that fail to adopt new production methods will be displaced by those that do.

The Bessemer converter displaced iron manufacturing. The open hearth furnace displaced Bessemer converters. Companies that clung to older technology faced bankruptcy, while Carnegie and Frick continuously upgraded.

Continuously invest in new technology, even if it means scrapping recent major investments. Technological leverage compounds over time.

Carnegie scrapped hundreds of thousands of dollars in recently purchased Bessemer converters when the open hearth furnace became available, because he understood that even marginal cost reductions would justify the capital expense.

“Even if we save half a dollar per ton by the changes, it would justify a large additional expenditure now.”

Learn skills outside your current job description during spare time. You never know when these skills will create unexpected opportunities or open doors to your life's work.

While sweeping the office floor, Carnegie taught himself to operate the telegraph by practicing on the instrument before operators arrived. This skill led him to meet Thomas Scott, work on the Pennsylvania Railroad, and eventually enter steel manufacturing. He credits this opportunistic learning as foundational.

“Whenever one learns to do anything, he has never to wait long for an opportunity of putting his knowledge to use.”

Invest in new technology immediately when it offers significant cost savings, even though the upfront expenditure appears large. The compound savings over the machine's lifetime far exceed the initial investment.

Older Pittsburgh manufacturers criticized Carnegie for spending heavily on new furnaces. But Carnegie calculated that new furnaces saved nearly half the waste in heating materials, justifying costs many times over. While competitors saw only the price, he saw the lifetime savings.

“In the heating of great masses of material, almost half the waste could sometimes be saved by using the new furnaces. The expenditure would have been justified even if it had been doubled.”

Respond to technological revolutions rather than being run over by them. Those who recognize and embrace new technologies gain permanent competitive advantage, while those who cling to old methods face obsolescence.

Carnegie's father was devastated when textile looms became obsolete. Young Carnegie witnessed this and resolved that he would not make the same mistake. Throughout his career, he was an early adopter of the Bessemer process for steel, employed chemists before competitors, invested in new furnaces, and was always several years ahead of the market.

“And then and there came the resolve that I would cure that when I got to be a man.”

leadership

High disagreeableness is an underrated entrepreneurial trait. The willingness to argue, push back, and deviate from expected paths is necessary to build something new when the world tells you it is impossible.

Carnegie earned a reputation as an argumentative and combative child who questioned authority. Rather than viewing this negatively, he recognized this trait developed his ability to persist against external pressure. This disagreeable nature enabled him to pursue unconventional paths that others dismissed.

“I earned the reputation of being an awful laddie. In this way, I probably developed a strain of argumentativeness or perhaps combativeness, which has always remained with me.”

Your greatest asset is the ability to organize and lead people, not technical mastery of your product. Success comes from understanding human nature and choosing people better than yourself.

Carnegie's first business venture was organizing childhood friends to gather rabbit food in exchange for naming rights to rabbits. Looking back, he credited this as evidence of his organizing power. He later realized he did not understand steam machinery but invested in understanding the more complicated mechanism of man.

“A success not to be attributed to what I have known or done myself, but to the faculty of knowing and choosing others who did know better than myself.”

When mentors or supervisors trust you with authority, step beyond your formal duties. Show you can make sound decisions independently and you will be given increasing responsibility.

When Thomas Scott was late to the office during a railroad crisis, Carnegie had to decide whether to issue an order under Scott's name. He took the risk and later found through Scott's actions that it was the right call. This demonstrated judgment and led Scott to trust him with more decisions.

“The battle of life is already half won by the young man who was brought personally in contact with high officials. The great aim of every boy should be to do something beyond the sphere of his duties, which attracts the attention of those over him.”

Frameworks

Cost Control as Permanent Advantage

Treat cost reduction as the primary metric, not revenue or profit. Track costs obsessively (down to the penny), reinvest savings into technology that drives further cost reduction, and understand that cost savings compound permanently while revenue and profit are cyclical. This creates a widening moat over time as competitors cannot match your structural cost advantage.

Use case: Manufacturing-intensive businesses competing on price or requiring continuous efficiency improvements

Downturn Acquisition Strategy

When markets contract and competitors face bankruptcy, deploy capital to acquire assets at steep discounts (25-50 percent below normal valuation). These assets, combined with your operational efficiency, create dominant market positions once recovery occurs. The key is having cash reserves and conviction that downturns are temporary.

Use case: Capital-intensive industries with cyclical demand; applies during recessions when asset prices crater

Vertical Integration by Degree

Do not automatically integrate backward into raw materials. First, test whether you can produce materials more cheaply internally than buying from external suppliers. If external suppliers have structural cost advantages, buy from them and use capital elsewhere. Integrate only when you have genuine efficiency advantages that create sustainable cost savings.

Use case: Manufacturing businesses considering backward integration into supplier industries

Controlled Partnership Equity

Acquire significant equity (but not majority control) in allied industries to secure supply or distribution advantages without operating the business yourself. This reduces capital requirements, provides cost benefits, and generates dividend income without management distraction.

Use case: Scaling companies seeking supply security or market leverage without full operational control

Acquisition as Market Entry

Enter competitive markets by creating a credible competing firm, then accept acquisition by the dominant player or merge with another competitor. The goal is not long-term operation but strategic positioning. Organize sufficiently to appear credible, negotiate from a position of threat, then execute the exit.

Use case: Entrepreneurs with limited capital entering industries dominated by entrenched competitors

Technological Moat Reinforcement

Continuously identify the next-generation technology before it becomes standard. Adopt it even if you must depreciate recent major investments. The cost of obsolescence far exceeds the cost of premature replacement. This keeps you perpetually ahead of competitors and prevents disruption.

Use case: Industries with predictable technology advancement cycles (manufacturing, software infrastructure, capital equipment)

The Grand Rule of Life

Fear only your own self-reproach, not others' judgment. The internal judge sits in the supreme court and cannot be cheated. You know whether you are putting forth your best effort and maintaining integrity. This principle frees you from external pressure and enables calm decision-making based on your own conscience rather than others' opinions.

Use case: When facing criticism or pressure to compromise values, or when anxiety about judgment is paralyzing decision-making.

Cost Accounting System

Implement weighing and accounting that tracks the cost of each process and the output of each person. This creates transparency impossible for competitors to replicate. Managers resist initially, but eventually the system pays dividends through detected waste and documented performance differences.

Use case: Scaling a manufacturing or operations business where cost reduction and efficiency are competitive advantages.

One Basket, Watch It Carefully

Concentrate all capital, time, and attention on mastering one business rather than diversifying across many. This requires believing you can manage your capital better than any board or external advisor. The focused approach allows you to become the best in your field and capture the true gold.

Use case: When deciding between diversifying and doubling down on your core business. Best applied when you have identified a business you can dominate.

The Internal Compass

Use your internal sense of right and wrong as the primary guide. You cannot control what others think, and external validation is unreliable. The only judgment that matters long-term is whether you can respect yourself and sleep soundly knowing you did right.

Use case: When facing pressure to compromise ethics or cut corners, or when seeking approval from people whose judgment you do not fully trust.

Stories

Carnegie worked as a bobbin boy earning $1.20 per week. Within a few years, through telegraph work and relationships, he made $35 per month, a 700x increase in annual income. His first dividend from Adams Express (10 dollars) matched two months of bobbin-boy wages and revealed the power of capital returns over labor.

Lesson: Wealth compounds when you transition from trading labor for income to deploying capital for returns. The earlier you recognize this and position yourself to capture capital returns, the faster you build wealth. Relationships and insider information accelerate the transition.

Carnegie built telegraph companies with no intention of operating them long-term. He would organize them as credible competitors to Western Union, then negotiate acquisition or merger at high multiples. In one case, he tripled his holdings in a merger without stringing a single wire. He used this as a stepping stone to bigger exits.

Lesson: You do not need to build a sustainable long-term business to create wealth. Strategic positioning and credible threats can generate high-multiple exits. The key is appearing credible while controlling your actual capital deployment.

During the Panic of 1873, while 360 railroad companies went bankrupt and one-sixth of the workforce lost jobs, Carnegie and Frick both deployed capital to acquire assets at 25 percent discounts. These bargain acquisitions, combined with their operational efficiency, positioned them as dominant suppliers once the market recovered.

Lesson: Economic downturns separate the winners from the losers. Winners are those with cash reserves and conviction, who view crisis as opportunity. Losers are those with high leverage and no dry powder. The best time to build competitive advantage is when others are desperate.

In 1887, Carnegie insisted on fixing the company book value at 50 million dollars despite its true market value of 200-250 million. When Frick wanted to exit, the ironclad agreement forced him to accept book value payouts in installments. Thirteen years later, when Frick found external buyers and attempted to sell the company at 250 million, Carnegie demanded a 2 million dollar non-refundable option fee to block the deal. Both sides' ego prevented a rational negotiation.

Lesson: Contractual rigidity creates incentives for one party to leave the partnership. If you lock in terms that do not reflect changing market reality, the other party will either attempt to exit or seek ways to undermine the agreement. Flexibility and periodic renegotiation preserve partnerships.

As a young child in Scotland, Carnegie organized his friends to gather food for rabbits every Saturday for an entire season. He offered no monetary payment, only the promise that the rabbits would be named after them. Looking back, he was ashamed of the hard bargain he drove, yet the friends willingly worked because the non-monetary reward satisfied them.

Lesson: Non-monetary rewards and recognition can motivate people powerfully. The ability to organize others around a vision is the most valuable business skill. This early experience taught Carnegie that organizing humans is more valuable than technical knowledge.

While working in a Pittsburgh factory basement, Carnegie was forced to inhale noxious fumes and oil that made him sick and caused him to vomit. Instead of despair, he reframed it optimistically, saying if he lost his appetite for lunch, he would have a better appetite for supper and the work would be done.

Lesson: Maniacal optimism and reframing are skills that can sustain you through difficult circumstances. Your perspective on hardship matters more than the hardship itself. This optimism is not denial but finding the upside while still doing the work.

When Thomas Scott was late to the office during a railroad crisis, Carnegie faced a decision: issue a necessary order under Scott's name without authorization, or wait and risk worsening the situation. He took the risk and issued the order. When Scott arrived, Carnegie confessed. Scott said nothing, but his actions later showed he believed Carnegie made the right call.

Lesson: Sometimes you must take intelligent risks beyond your formal authority to serve the mission. Show sound judgment in these moments and you will be trusted with increasing authority. Your ability to decide wisely when it matters most is what leaders recognize.

Colonel James Anderson, an older man Carnegie did not know well, opened his library of 400 volumes to local boys, allowing each to borrow one book per week. This act of kindness transformed Carnegie's life and access to knowledge. Decades later, he funded hundreds of public libraries, explicitly crediting Anderson's generosity as the inspiration.

Lesson: Small acts of kindness and generosity can profoundly impact someone's trajectory. The ripple effects of giving compound across decades and influence how recipients later give to others. Your kindness may shape a future leader.

Carnegie was offered an office job in Pittsburgh by the Pennsylvania Railroad. When asked when he could start, he said he could start immediately and right now if needed. Looking back, he recognized this instant acceptance was crucial because something might have changed or another candidate might have been found.

Lesson: When opportunity knocks, answer immediately. Delay costs. The window for seizing an opportunity is often narrower than you think. Those who act decisively without overthinking often capture doors others lose.

At age 10, Carnegie was tasked with feeding his family's pigeons and rabbits but lacked time to forage for food himself. He convinced other children to collect dandelions and clover by offering to name the animals after them. He created a system where others provided the labor while he managed the operation.

Lesson: Early evidence of organizational ability. Success comes from knowing how to attract capable people and orchestrate their efforts toward a goal, not from doing all the work yourself. This pattern, established in childhood, became his core strength as a business leader.

Notable Quotes

“Cut the prices scoop the market the costs, and the profits will take care of themselves.”

Describing his philosophy of cost control as the primary driver of competitive advantage. Unlike competitors focused on revenue, Carnegie obsessed over expense reduction.

“The best time to expand was when no one else dared to take the risks.”

Explaining his strategy during economic downturns. He and Frick both deployed capital during the Panic of 1873 to acquire assets at 25 percent discounts.

“Even if we save half a dollar per ton by the changes, it would justify a large additional expenditure now.”

Justifying the scrapping of recently installed Bessemer converters to adopt the newer open hearth furnace. Demonstrates his long-term thinking about technology adoption.

“Man must have an idol. The amassing of wealth is one of the worst species of idolatry no idol more debasing than the worship of money.”

Written to himself at age 28, expressing internal conflict between his religious upbringing and his overwhelming ambition. He promised to retire at 35 but never did.

“I will resign business at 35.”

A pledge he made to himself in his twenties but was too ambitious to honor. He continued accumulating wealth until selling his company at age 65.

“Eureka, I cried. Here's the goose that lays the golden egg.”

Reaction to receiving his first dividend check (10 dollars) from Adams Express. This single check exceeded two months of bobbin-boy wages and shaped his lifelong investment philosophy.

“Profits and prices are cyclical subject to any number of transient forces of the marketplace. Cost however could be strictly controlled.”

Core principle underlying his competitive strategy. He understood that permanent advantage came from cost control, not from chasing revenue or profit cycles.

“A sunny disposition is worth more than a fortune. Young people should know that it can be cultivated, that the mind, like the body, can be moved from the shade into sunshine.”

Early in his autobiography, Carnegie reflects on his optimistic nature and offers advice to young people about cultivating optimism as a learnable skill.

“Thine own reproach alone do fear. This motto adopted early in life has been more to me than all sermons I have ever heard.”

Carnegie describes his grand rule of life, emphasizing that internal integrity and self-respect matter more than external judgment.

“I remember that shortly after this, I began to learn what poverty meant. Then and there came the resolve that I would cure that when I got to be a man.”

Reflecting on his childhood when his father lost his job to technological displacement and the family fled Scotland to America.

Frequently Asked Questions

What are Andrew Carnegie's key business principles?▼

Andrew Carnegie's core principles include: Identify where competitors are making mistakes and turn that into competitive advantage. Mediocrity in competitors creates opportunities for those willing to do things differently.. Use price reductions as a lever to increase market share and scale, knowing that lower costs create a virtuous cycle of volume growth.. Involve younger team members or family in financial understanding. Transparency about income, expenses, and goals creates shared responsibility and teaches financial discipline early.. Founder Almanac has cataloged 30 total principles from Andrew's career.

What can entrepreneurs learn from Andrew Carnegie?▼

Key lessons from Andrew Carnegie include: Wealth compounds when you transition from trading labor for income to deploying capital for returns. The earlier you recognize this and position yourself to capture capital returns, the faster you build wealth. Relationships and insider information accelerate the transition.. Explore 10 stories and 10 frameworks from Andrew's experience.

What is Andrew Carnegie known for in business?▼

A pioneering industrialist, Andrew Carnegie transformed the steel industry through his establishment of Carnegie Steel Company, which became the largest of its kind in the world by the late 19th century. Rising from humble beginnings as a bobbin boy earning just $1.20 per week, he leveraged technological advancements and strategic partnerships to amass a fortune, ultimately selling his steel company for $480 million in 1901. Carnegie's principles emphasized the importance of adapting to industry dynamics and recognizing the necessity of innovation, famously stating, "Cut the prices scoop the market the costs, and the profits will take care of themselves." His journey illustrates the critical balance between emotional attachment and rational decision-making in business, offering valuable lessons for entrepreneurs today.

More Manufacturing Founders

Want Andrew's advice on your business?

Our AI has studied Andrew Carnegie's biography, principles, and decision-making frameworks. Ask any business question.

Start a conversation